Key Takeaways:

- Following last week’s rejection of Theresa May’s Brexit plan, we discuss what’s next for the United Kingdom and possible market implications.

- We maintain a cautious tactical view on European equities, given lackluster economic growth, increased political risk, and only fair valuations.

- A better economic and earnings growth outlook and a possible pause in Federal Reserve rate hikes underpin our preference for emerging market equities.

Brexit uncertainty continues to cloud Europe’s economy. On January 15, more than two-thirds of the U.K. Parliament voted against British Prime Minister Theresa May’s European Union (EU) separation deal, another bump in the road for “Brexit.” That outcome had been anticipated, though the wide margin underscored the tough road ahead. Even though May survived a no-confidence vote the next day, the margin was narrow, and the path forward remains unclear. Here we discuss potential market implications of the United Kingdom’s ongoing effort to leave the EU. We also share our updated views on European equities and reiterate our preference for emerging market (EM) equities over developed international equities.

Brexit: Now What?

As we write this, May is negotiating with opposition and coalition parties, and will attempt to strike an amended deal. At this point, we find it difficult to envision a cross-party agreement—a so-called “soft Brexit”—and are skeptical that any deal will be struck by the March 29 deadline. As a result, the odds have increased that the U.K. may end up staying in the European Union, potentially via a second referendum. Our best guess at this point is that a negotiated “soft Brexit” deal eventually may be reached, but it may take beyond March. Still, a second referendum, a hard Brexit (leaving without any deal), or regime change remain on the table. Should the U.K. go down the hard Brexit path, the U.K. economy would likely slow further as EU trade uncertainty weighs on consumer sentiment and business investment. Over the past year, economic growth expectations for the U.K. have fallen only marginally (Bloomberg consensus is calling for lackluster 1.3% gross domestic product [GDP] growth in 2018), while forecasts for 2019 have held steady at 1.5%. Manufacturing activity has held steady throughout the more than two-year ordeal, in part because of the weakness in the British pound.

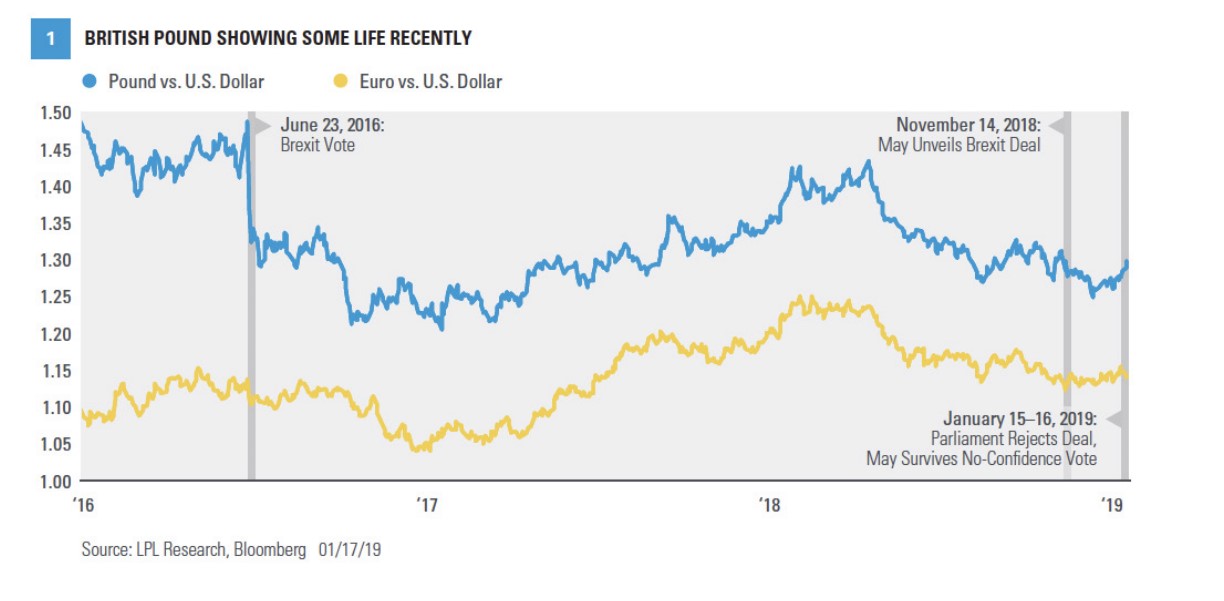

Recent strength in the British currency [Figure 1], which has been sensitive to Brexit headlines, is somewhat reassuring. The U.K. constitutes only about 2% of the global economy and 4% of world goods trade, so global ramifications of all realistic scenarios are likely to be manageable. Economic forecasting firm Capital Economics thinks a disorderly exit could cause a 1–2% hit to British GDP growth, spread over two years.

Broader International Outlook

Lackluster economic growth, heightened political risk, and—despite weakness—only fair valuations drive our cautious tactical view of European equities. Europe, including the U.K., represents the bulk of the international developed markets, and is wrestling with some of the globe’s biggest policy issues. A tighter regulatory environment, labor laws that restrict business growth, and the rise of populism throughout Europe remain structural concerns.

Beyond Brexit, which has clearly hurt the U.K. stock market [Figure 2], Italy still has a debt and spending problem that will likely fare up again for the world’s third-largest bond market. Even Europe stalwart Germany appears to have narrowly avoided slipping into an economic recession in the fourth quarter (defined as two consecutive quarters of contraction in GDP) and grew only 1% over the past year. More broadly, in developed international equity markets (including Japan and other major non- European markets), the picture improves some. Still, even with the lift from faster-growing Asian economies, we do not expect GDP growth in international developed economies to reach 2% in 2019, supporting our cautious tactical stance toward developed international markets. We believe the outlook for EM is better. Economic growth in emerging market economies may approach 5% in 2019, based on Bloomberg’s consensus forecast, while high-single-digit earnings growth is achievable in our view. Other potential catalysts include a likely first-half pause in the Federal Reserve’s rate hike campaign, U.S. dollar weakness, and a U.S.-China trade agreement. In the meantime, China will likely launch more stimulus programs to help stabilize growth. More fare-ups in fiscally challenged EM countries and escalating trade tensions are possible, but we’re comfortable with these risks, particularly given attractive EM valuations.

Conclusion

Brexit uncertainty continues to cloud the growth outlook for the U.K. and has the potential to weigh on consumer sentiment and business investment throughout Europe. We continue to favor U.S. and EM equities over their developed international counterparts for tactical global equity allocations. Among developed markets, the United States remains the standout in terms of economic and earnings growth, while we continue to see solid upside potential in EM.

Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful. Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market. Investing in foreign securities involves special additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks. All investing involves risk including loss of principal.

DEFINITIONS Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments, and exports less imports that occur within a defined territory. INDEX DESCRIPTIONS The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey. The MSCI All Country World Index is an unmanaged, free float-adjusted, market capitalization-weighted index composed of stocks of companies located in countries throughout the world. It is designed to measure equity market performance in global developed and emerging markets. The index includes reinvestment of dividends, net of foreign withholding taxes. The MSCI EAFE Index is made up of approximately 1,045 equity securities issued by companies located in 19 countries and listed on the stock exchanges of Europe, Australia, and the Far East. All values are expressed in U.S. dollars. Past performance is no guarantee of future results.

This research material has been prepared by LPL Financial LLC. To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Investment advice offered through Shepherd Financial Partners, LLC, a registered investment advisor. Securities offered through LPL Financial, member FINRA/SIPC. Shepherd Financial Partners and LPL Financial are separate entities. Tracking #1-814053